The Supreme Court’s recent refusal to hear Murrin v. Commissioner left in place a Third Circuit ruling with serious consequences for taxpayers. It also raised a broader question that often comes up when federal courts make news: how far does one circuit court’s ruling actually reach?

In Murrin, a tax preparer included false or fraudulent entries on the taxpayer’s returns. The preparer also omitted his name and signature from the preparer line, listed different entities as the preparer from year to year, used different post office boxes as business addresses on partnership returns, and caused partnership returns to be mailed to different IRS service centers.

Years later, long after the ordinary three-year period had expired, the IRS sought to assess about $328,000 in tax, penalties, and interest (the interest alone was more than $250,000 by the time the IRS issued the notice of deficiency).

Murrin challenged the assessment, claiming that the statute of limitations had already run. The IRS argued that because the returns were fraudulent, the usual three-year deadline did not apply. The Tax Court agreed with the IRS, and on appeal, the Third Circuit did, too.

(You can read more about the case here.)

What Is A Circuit Court?

When people refer to a “circuit court” in the federal system, they usually mean a U.S. Court of Appeals. These courts sit between the federal district courts and the U.S. Supreme Court.

Most federal cases begin in a district court, which is the trial-level court. That’s where the parties build the record, including testimony from witnesses and the introduction of evidence. In some cases, there may also be a trial (it’s worth noting that cases are often argued on paper more than in person).

If one side believes the district court got the law wrong, they can appeal it to the court of appeals. But an appeal is not a second trial. The court of appeals generally does not hear new witnesses, take new evidence, or retry the facts. Its job is to review what happened below and decide whether the law was applied correctly.

A circuit court may affirm the lower court’s decision, reverse it, vacate it, or remand the case for further proceedings. When a case is sent back, or remanded, the lower court usually receives instructions about what should happen next.

Circuit courts also create precedent. When a circuit court interprets federal law, lower federal courts within that circuit generally have to follow that interpretation unless the Supreme Court says otherwise.

That’s why the Third Circuit’s ruling in Murrin matters: lower federal courts within that circuit generally must follow it unless the Supreme Court or the Third Circuit later changes course.

Does A Circuit Court Ruling Apply Everywhere?

A circuit court ruling generally binds only the federal courts within that circuit. That means a Third Circuit decision binds federal district courts in the Third Circuit. It does not automatically control what happens in the Fourth Circuit, Fifth Circuit, Ninth Circuit, or any other circuit.

The distinction is important. If the Third Circuit decides a tax issue one way, a taxpayer in Pennsylvania may face a different legal landscape than a taxpayer in California, Texas, or Florida. Courts outside the Third Circuit may still look at the decision and find it persuasive, but they are not required to follow it simply because the Third Circuit said so.

That means the same federal statute may be interpreted one way in one part of the country and differently in another.

Why Are They Called Circuit Courts?

The name comes from the way the federal court system is organized. The country is divided into regional circuits, and each circuit has its own court of appeals.

So when you hear someone refer to the Third Circuit or Ninth Circuit, they are talking about the federal appellate court for a particular part of the country.

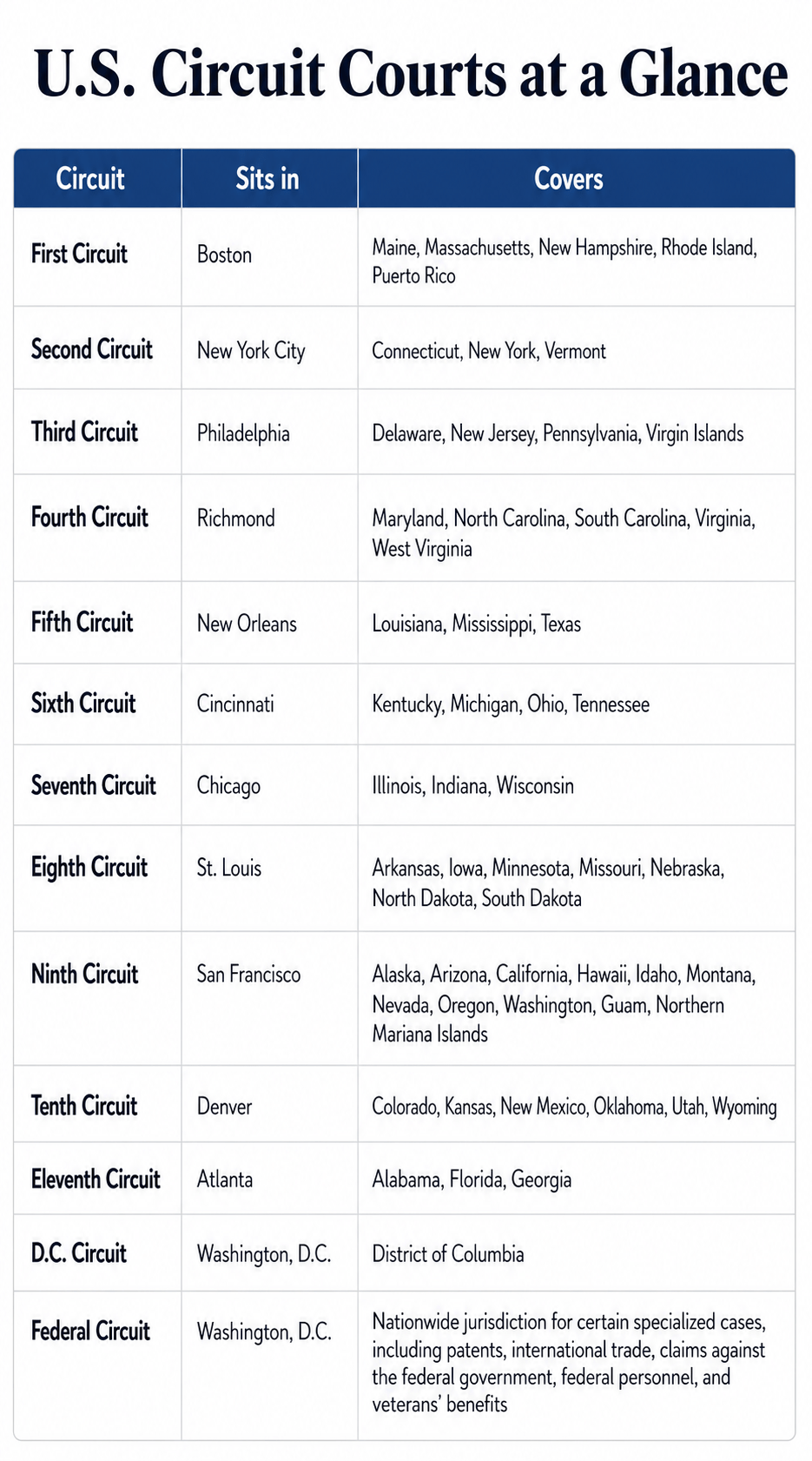

Here’s a quick summary:

The Federal Circuit also sits in Washington, D.C., but it is different from the regional circuits. Its jurisdiction is largely based on subject matter rather than geography. That includes appeals from the Court of Federal Claims, which can hear federal tax refund suits after the taxpayer has paid the disputed amount. Refund suits filed in federal district court, by contrast, generally go to the regional circuit for that district.

What Is a Circuit Split?

A circuit split happens when different federal courts of appeals reach different conclusions on the same question of federal law.

That was part of the argument in Murrin. Murrin claimed that the Third Circuit had split from the Federal Circuit’s earlier decision in BASR Partnership v. United States, which held that the fraud exception applies only when the taxpayer, not a third party, acted with intent to evade tax.

Circuit splits matter because they can make a case more likely to attract the Supreme Court’s attention. The Supreme Court does not take most cases, but when federal law means one thing in one part of the country and something else in another, that disagreement can be a reason for review.

Even then, review is not guaranteed. In Murrin, the Supreme Court declined to hear the case.

What Does It Mean When the Supreme Court Denies Cert?

When a party asks the Supreme Court to hear a case, that request is called a petition for a writ of certiorari. If the Court agrees to hear the case, it grants cert. If it declines, it denies cert.

A denial of cert does not mean the Supreme Court agrees with the lower court. It does not make the lower court’s decision the law of the entire country. It simply means the Supreme Court is not taking that case.

That is what happened in Murrin. The Third Circuit’s ruling remains in place, but the Supreme Court did not endorse it.

Can a Circuit Court Ruling Still Matter Outside Its Circuit?

A circuit court decision may not bind the entire country, but it can still influence what happens elsewhere. Other courts may treat it as persuasive authority, federal agencies may rely on it when litigating similar cases, and taxpayers and advisers may adjust their risk calculations once a circuit court has accepted a particular argument.

That is especially true in tax cases. A win for the IRS in one circuit can shape how the government approaches similar disputes before other circuits have weighed in. A taxpayer outside the Third Circuit may not be bound by Murrin in the same way, but the case still signals how the IRS may argue the issue.

What Does It All Mean?

Circuit courts are powerful because, for most federal cases, they are the last meaningful stop. The Supreme Court hears only a small fraction of the cases it is asked to review, so a court of appeals decision often becomes the final word for the parties.

But that does not mean every circuit court decision applies nationwide. Most of the time, a circuit court ruling binds the courts within that circuit and serves as persuasive authority elsewhere.

That is why Murrin matters, but also why the Supreme Court’s denial should not be mistaken for a nationwide rule. The Supreme Court did not bless the Third Circuit’s reasoning—it left the ruling in place. For taxpayers in the Third Circuit, that is enough. But for taxpayers elsewhere, it is a warning sign—and possibly a preview of the next fight.